cffilter

Syntax

Description

The cffilter function applies the Christiano-Fitzgerald filter to

separate one or more time series into additive trend and cyclical components.

cffilter optionally plots the series and trend component, with

cycles removed.

In addition to the Christiano-Fitzgerald filter, Econometrics Toolbox™ supports the Baxter-King (bkfilter), Hamilton

(hfilter), and

Hodrick-Prescott (hpfilter) filters.

[

returns tables or timetables containing variables for the trend and cyclical components

from applying the Christiano-Fitzgerald filter to each variable in an input table or

timetable. To select different variables to filter, use the

TTbl,CTbl] = cffilter(Tbl)DataVariables name-value argument.

[___] = cffilter(___,

specifies options using one or more name-value arguments in

addition to any of the input argument combinations in previous syntaxes.

Name=Value)cffilter returns the output argument combination for the

corresponding input arguments. For example, cffilter(Tbl,Symmetric=true,Drift=[false false

true],DataVariables=1:3) applies the symmetric Christiano-Fitzgerald filter to

the first three variables in the input table Tbl, and removes the

linear drift term from the third variable before applying the filter.

cffilter(___) plots time series variables in the

input data and their respective smoothed trend components (cycles removed), computed by

the Christiano-Fitzgerald filter, on the same axes.

cffilter(

plots on the axes specified by ax,___)ax instead of

the current axes (gca). ax can precede any of the input

argument combinations in the previous syntaxes.

Examples

Plot the cyclical component of the US post-WWII, seasonally adjusted, quarterly, real gross national product (GNPR).

load Data_GNP

GNPR = Data(:,2);

[trend,cyclical] = cffilter(GNPR);

T = numel(trend)T = 235

trend and cyclical are 235-by-1 vectors containing the trend and cyclical components, respectively, resulting from applying the asymmetric Christiano-Fitzgerald filter to the series with default upper and lower cutoffs.

plot(dates,cyclical) axis tight ylabel("Real GNP Cyclical Component")

Apply the Christiano-Fitzgerald filter to all variables in input table variables.

Load the Schwert stock data set Data_SchwertStock.mat, which contains monthly returns of the NYSE index from 1871 through 2008 in DataTimeTableMth, among three other variables (for details, enter Description). Remove all missing observations from all series.

load Data_SchwertStock

TTM = rmmissing(DataTimeTableMth);Aggregate the monthly data in the timetable to quarterly measurements.

TTQ = convert2quarterly(TTM);

Apply the asymmetric Christiano-Fitzgerald filter to all variables in the quarterly timetable. Use the default cutoffs.

[TQTT,CQTT] = cffilter(TTQ); size(TQTT)

ans = 1×2

220 4

TQTT and CQTT are 220-by-4 timetables containing the trend and cyclical components, respectively, of the series in TTQ. Variables in the input and output timetables correspond. By default, cffilter filters all variables in the input table or timetable. To select a subset of variables, set the DataVariables option.

To compare outputs between different tabular inputs, apply the Christiano-Fitzgerald filter to all variables in the table of monthly data DataTableMth and the timetable of monthly data TTM.

% Table input of daily data

DTM = rmmissing(DataTableMth);

[TMDT,CMDT] = cffilter(DTM);

size(TMDT)ans = 1×2

656 4

tail(TMDT)

Return DivYld CapGain CapGainA

__________ _________ __________ __________

May1925 0.082825 0.0030391 0.079846 0.079786

Jun1925 0.005878 0.0057145 0.00023547 0.00016356

Jul1925 0.014371 0.0054548 0.0089194 0.0089158

Aug1925 0.046424 0.0033349 0.043012 0.04309

Sep1925 0.022868 0.0064024 0.016375 0.016465

Oct1925 0.079477 0.0058413 0.073612 0.073636

Nov1925 0.00055416 0.003497 -0.0028871 -0.0029429

Dec1925 0.050338 0.0068429 0.043564 0.043495

tail(CMDT)

Return DivYld CapGain CapGainA

__________ ___________ __________ ___________

May1925 -0.016639 -0.00055599 -0.016143 -0.016083

Jun1925 -0.0026377 -0.00025619 -0.0024535 -0.0023816

Jul1925 0.0044847 -0.00024249 0.0047236 0.0047272

Aug1925 0.0017835 -0.00062296 0.0024837 0.0024064

Sep1925 -0.0060897 -0.0011003 -0.0048985 -0.0049894

Oct1925 -0.011281 -0.0012017 -0.010055 -0.010079

Nov1925 -0.0090187 -0.00068252 -0.0083919 -0.0083361

Dec1925 -0.000747 0.00024995 -0.0010665 -0.00099695

% Timetable input of daily data

[TMTT,CMTT] = cffilter(TTM);

size(TMTT)ans = 1×2

656 4

tail(TMTT)

Time Return DivYld CapGain CapGainA

___________ __________ _________ __________ __________

01-May-1925 0.082825 0.0030391 0.079846 0.079786

01-Jun-1925 0.005878 0.0057145 0.00023547 0.00016356

01-Jul-1925 0.014371 0.0054548 0.0089194 0.0089158

01-Aug-1925 0.046424 0.0033349 0.043012 0.04309

01-Sep-1925 0.022868 0.0064024 0.016375 0.016465

01-Oct-1925 0.079477 0.0058413 0.073612 0.073636

01-Nov-1925 0.00055416 0.003497 -0.0028871 -0.0029429

01-Dec-1925 0.050338 0.0068429 0.043564 0.043495

tail(CMTT)

Time Return DivYld CapGain CapGainA

___________ __________ ___________ __________ ___________

01-May-1925 -0.016639 -0.00055599 -0.016143 -0.016083

01-Jun-1925 -0.0026377 -0.00025619 -0.0024535 -0.0023816

01-Jul-1925 0.0044847 -0.00024249 0.0047236 0.0047272

01-Aug-1925 0.0017835 -0.00062296 0.0024837 0.0024064

01-Sep-1925 -0.0060897 -0.0011003 -0.0048985 -0.0049894

01-Oct-1925 -0.011281 -0.0012017 -0.010055 -0.010079

01-Nov-1925 -0.0090187 -0.00068252 -0.0083919 -0.0083361

01-Dec-1925 -0.000747 0.00024995 -0.0010665 -0.00099695

Because the data is disaggregated, the outputs of the daily data have more rows than from the quarterly data. The filter results of the daily inputs are equal among the corresponding outputs, but cffilter returns tables of results, instead of timetables, when you supply data in a table.

Load the Nelson-Plosser macroeconomic data set Data_NelsonPlosser.mat, which contains series measured yearly in the timetable DataTimeTable.

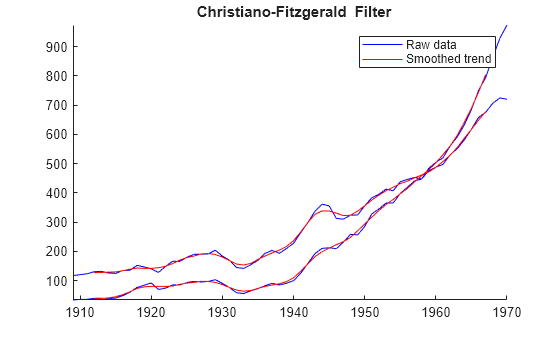

load Data_NelsonPlosserApply the asymmetric Christiano-Fitzgerald filter to the real and nominal GNP series, GNPR and GNPN, respectively. Filter out cyclical component frequencies outside the interval [2,8]. Plot the trend component with each series.

figure cffilter(DataTimeTable,DataVariables=["GNPR" "GNPN"], ... LowerCutoff=2,UpperCutoff=8);

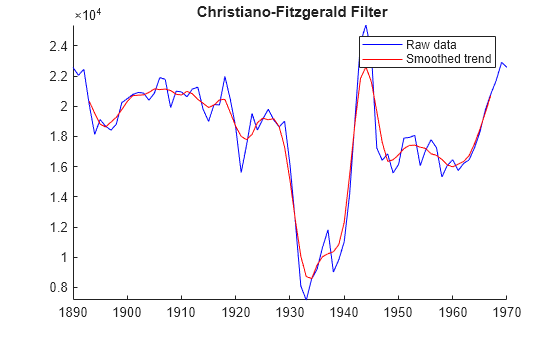

Compare the results of the asymmetric filter with the symmetric filter. in addition to cyclical component cutoffs of 2 and 8, and set the lag length of the symmetric moving average to 3 years.

figure cffilter(DataTimeTable,DataVariables=["GNPR" "GNPN"], ... LowerCutoff=2,UpperCutoff=8,FilterType="symmetric",LagLength=3);

Unlike the asymmetric filter, the first and last LagLength=3 values of the returned components of the symmetric filter are NaN-valued.

Experiment with filter parameter values by adjusting the interactive controls. Because this setup always sets the lag length of the symmetric moving average, cffilter implements the symmetric method only.

varnames = string(DataTimeTable.Properties.VariableNames); lc =2; % LowerCutoff uc =

8; % UpperCutoff q =

3; % LagLength tfs =

false; % Stationarity tfd =

true; % Drift vn =

varnames(5); % DataVariables figure [TTbl,CTbl,h] = cffilter(DataTimeTable,DataVariables=vn, ... LowerCutoff=lc,UpperCutoff=uc,LagLength=q,Stationarity=tfs, ... Drift=tfd);

Input Arguments

Name-Value Arguments

Output Arguments

More About

Tips

The definition of a business cycle in [1]

suggests values in the table for the cutoff periods LowerCutoff and

UpperCutoff, and lag length LagLength that depend

on the periodicity of the data.

| Periodicity | LowerCutoff | UpperCutoff | LagLength |

|---|---|---|---|

| Yearly | 2 | 8 | 3 |

| Quarterly | 6 | 32 | 12 |

| Monthly | 18 | 96 | 36 |

In practice, use vectors of cutoff periods and lag lengths to test alternatives. Use the

plot produced by cffilter to compare results among settings.

References

Version History

Introduced in R2023a