simByTransition

Simulate CIR sample paths with transition

density

Description

[

simulates Paths,Times] = simByTransition(MDL,NPeriods)NTrials sample paths of NVars

independent state variables driven by the Cox-Ingersoll-Ross (CIR) process sources

of risk over NPeriods consecutive observation periods.

simByTransition approximates a continuous-time CIR model

using an approximation of the transition density function.

[

specifies options using one or more name-value pair arguments in addition to the

input arguments in the previous syntax.Paths,Times] = simByTransition(___,Name,Value)

You can perform quasi-Monte Carlo simulations using the name-value arguments for

MonteCarloMethod, QuasiSequence, and

BrownianMotionMethod. For more information, see Quasi-Monte Carlo Simulation.

Examples

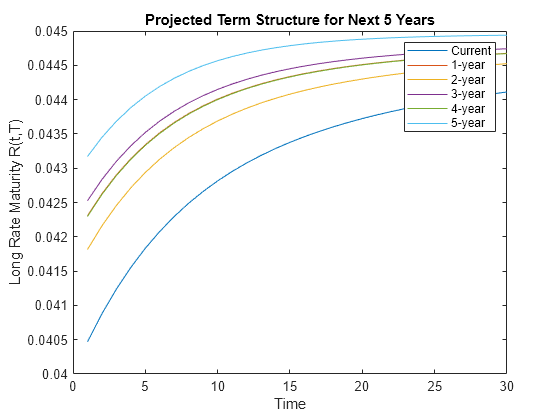

Using the short rate, simulate the rate dynamics and term structures in the future using a CIR model. The CIR model is expressed as

The exponential affine form of the bond price is

where

and

Define the parameters for the cir object.

alpha = .1; b = .05; sigma = .05; r0 = .04;

Define the function for bond prices.

gamma = sqrt(alpha^2 + 2*sigma^2); A_func = @(t, T) ... 2*(exp(gamma*(T-t))-1)/((alpha+gamma)*(exp(gamma*(T-t))-1)+2*gamma); C_func = @(t, T) ... (2*alpha*b/sigma^2)*log(2*gamma*exp((alpha+gamma)*(T-t)/2)/((alpha+gamma)*(exp(gamma*(T-t))-1)+2*gamma)); P_func = @(t,T,r_t) exp(-A_func(t,T)*r_t+C_func(t,T));

Create a cir object.

obj = cir(alpha,b,sigma,'StartState',r0)obj =

Class CIR: Cox-Ingersoll-Ross

----------------------------------------

Dimensions: State = 1, Brownian = 1

----------------------------------------

StartTime: 0

StartState: 0.04

Correlation: 1

Drift: drift rate function F(t,X(t))

Diffusion: diffusion rate function G(t,X(t))

Simulation: simulation method/function simByEuler

Sigma: 0.05

Level: 0.05

Speed: 0.1

Define the simulation parameters.

nTrials = 100; nPeriods = 5; % Simulate future short over the next five years nSteps = 12; % Set intermediate steps to improve the accuracy

Simulate the short rates. The returning path is a (NPeriods + 1)-by-NVars-by-NTrials three-dimensional time-series array. For this example, the size of the output is 6-by-1-by-100.

rng('default'); % Reproduce the same result rPaths = simByTransition(obj,nPeriods,'nTrials',nTrials,'nSteps',nSteps); size(rPaths)

ans = 1×3

6 1 100

rPathsExp = mean(rPaths,3);

Determine the term structure over the next 30 years.

maturity = 30; T = 1:maturity; futuresTimes = 1:nPeriods+1; % Preallocate simTermStruc simTermStructure = zeros(nPeriods+1,30); for i = futuresTimes for t = T bondPrice = P_func(i,i+t,rPathsExp(i)); simTermStructure(i,t) = -log(bondPrice)/t; end end plot(simTermStructure') legend('Current','1-year','2-year','3-year','4-year','5-year') title('Projected Term Structure for Next 5 Years') ylabel('Long Rate Maturity R(t,T)') xlabel('Time')

The Cox-Ingersoll-Ross (CIR) short rate class derives directly from SDE with mean-reverting drift (SDEMRD):

where is a diagonal matrix whose elements are the square root of the corresponding element of the state vector.

Create a cir object to represent the model: .

cir_obj = cir(0.2, 0.1, 0.05) % (Speed, Level, Sigma)cir_obj =

Class CIR: Cox-Ingersoll-Ross

----------------------------------------

Dimensions: State = 1, Brownian = 1

----------------------------------------

StartTime: 0

StartState: 1

Correlation: 1

Drift: drift rate function F(t,X(t))

Diffusion: diffusion rate function G(t,X(t))

Simulation: simulation method/function simByEuler

Sigma: 0.05

Level: 0.1

Speed: 0.2

Define the quasi-Monte Carlo simulation using the optional name-value arguments for 'MonteCarloMethod','QuasiSequence', and 'BrownianMotionMethod'.

[paths,time] = simByTransition(cir_obj,10,'ntrials',4096,'montecarlomethod','quasi','quasisequence','sobol','BrownianMotionMethod','principal-components');

Input Arguments

Name-Value Arguments

Output Arguments

More About

There are inheritance relationships among the SDE classes.

The following figure illustrates the inheritance relationships.

For more information, see SDE Class Hierarchy.

Algorithms

Use the simByTransition function to simulate any vector-valued CIR

process of the form

where

Xt is an

NVars-by-1state vector of process variables.S is an

NVars-by-NVarsmatrix of mean reversion speeds (the rate of mean reversion).L is an

NVars-by-1vector of mean reversion levels (long-run mean or level).D is an

NVars-by-NVarsdiagonal matrix, where each element along the main diagonal is the square root of the corresponding element of the state vector.V is an

NVars-by-NBrownsinstantaneous volatility rate matrix.dWt is an

NBrowns-by-1Brownian motion vector.

References

[1] Glasserman, P. Monte Carlo Methods in Financial Engineering, New York: Springer-Verlag, 2004.