oobQuantileError

Out-of-bag quantile loss of bag of regression trees

Description

err = oobQuantileError(Mdl)Mdl.Y to the predicted,

out-of-bag medians at Mdl.X, the predictor data, and using the bag of

regression trees Mdl. Mdl must be a TreeBagger model object.

err = oobQuantileError(Mdl,Name,Value)Name,Value pair

arguments. For example, specify quantile probabilities, the error type, or which trees to

include in the quantile-regression-error estimation.

Input Arguments

Name-Value Arguments

Output Arguments

Examples

Load the carsmall data set. Consider a model that predicts the fuel economy of a car given its engine displacement, weight, and number of cylinders. Consider Cylinders a categorical variable.

load carsmall

Cylinders = categorical(Cylinders);

X = table(Displacement,Weight,Cylinders,MPG);Train an ensemble of bagged regression trees using the entire data set. Specify 100 weak learners and save the out-of-bag indices.

rng(1); % For reproducibility Mdl = TreeBagger(100,X,'MPG','Method','regression','OOBPrediction','on');

Mdl is a TreeBagger ensemble.

Perform quantile regression, and out-of-bag estimate the MAD of the entire ensemble using the predicted conditional medians.

oobErr = oobQuantileError(Mdl)

oobErr = 1.5349

oobErr is an unbiased estimate of the quantile regression error for the entire ensemble.

Load the carsmall data set. Consider a model that predicts the fuel economy of a car given its engine displacement, weight, and number of cylinders.

load carsmall

X = table(Displacement,Weight,Cylinders,MPG);Train an ensemble of bagged regression trees using the entire data set. Specify 250 weak learners and save the out-of-bag indices.

rng('default'); % For reproducibility Mdl = TreeBagger(250,X,'MPG','Method','regression',... 'OOBPrediction','on');

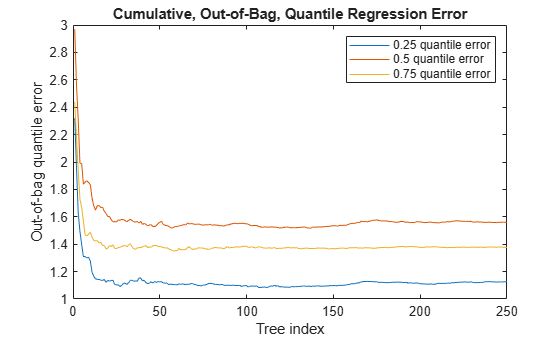

Estimate the cumulative; out-of-bag; 0.25, 0.5, and 0.75 quantile regression errors.

err = oobQuantileError(Mdl,'Quantile',[0.25 0.5 0.75],'Mode','cumulative');

err is an 250-by-3 matrix of cumulative, out-of-bag, quantile regression errors. Columns correspond to quantile probabilities and rows correspond to trees in the ensemble. The errors are cumulative, so they incorporate aggregated predictions from previous trees.

Plot the cumulative, out-of-bag, quantile errors on the same plot.

figure; plot(err); legend('0.25 quantile error','0.5 quantile error','0.75 quantile error'); ylabel('Out-of-bag quantile error'); xlabel('Tree index'); title('Cumulative, Out-of-Bag, Quantile Regression Error')

All quantile error curves appear to level off after training about 50 trees. So, training 50 trees appears to be sufficient to achieve minimal quantile error for the three quantile probabilities.

More About

Tips

The out-of-bag ensemble error estimator is unbiased for the true ensemble error. So, to tune parameters of a random forest, estimate the out-of-bag ensemble error instead of implementing cross-validation.

References

[1] Breiman, L. "Random Forests." Machine Learning 45, pp. 5–32, 2001.

[2] Meinshausen, N. “Quantile Regression Forests.” Journal of Machine Learning Research, Vol. 7, 2006, pp. 983–999.

Version History

Introduced in R2016b